401k Auto Enrollment – How Will You Embrace the Automatic Age?

Since the beginning of time, there have been several ages that reflect society propelling itself forward in physical, intellectual and technological ways. First, there was the Stone Age. Then came the Iron and Bronze Ages (not to mention the Golden Age and the Age of Enlightenment).

Since the beginning of time, there have been several ages that reflect society propelling itself forward in physical, intellectual and technological ways. First, there was the Stone Age. Then came the Iron and Bronze Ages (not to mention the Golden Age and the Age of Enlightenment).

Welcome to the Automatic Age… of the 401k

Section 101 of SECURE Act 2.0 requires new 401(k) and 403(b) plans to automatically enroll participants, with the initial automatic enrollment amount being at least 3% but not more than 10%. Each year, that amount must be automatically increased by 1% until it reaches at least 10%, but not more than 15%.1 However, plans that existed on or prior to the December 29, 2022, signing of the SECURE Act do not have to follow this new provision — they were grandfathered in.

Breaking Down the Grandfather Clause

Just how many plans are out there right now that haven’t yet embraced the Automatic Age? According to the Society for Human Resource Management’s 2022 Employee Benefits report2 (based on responses from 3,129 human resource professionals across the United States), only about a half of the plans automatically enroll new or existing employees, and only 26% automatically increase employee contributions annually. Vanguard’s “How America Saves 2022” report3 reveals that 56% of Vanguard plans have adopted automatic enrollment and two-thirds of those plans have implemented automatic annual deferral rate increases. PSCA’s 65th Annual Survey (most recent) puts those figures at 59% (auto-enroll) and 78% (auto-increase).

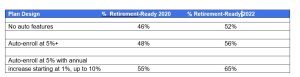

Embracing the Numbers

For several years now, the case has been made that automatic enrollment and escalation plan features work. According to a 2012 ground-breaking Ariel/Aon-Hewitt study, automatic enrollment helps workers who wouldn’t normally participate in a company’s retirement plan. “The most dramatic increases in enrollment rates are among younger, lower-paid employees, and the racial gap in participation rates is nearly eliminated among employees subject to auto-enrollment,” the study found.4 More recently, John Hancock’s “State of the participant 2022”5 report found that auto-enroll/auto-increase features used in tandem greatly enhance a participant’s chances of achieving retirement readiness.

The majority of surveys and research reports addressing automatic features show that adoption, usage and effectiveness are on the rise from previous years, which is cause for great optimism. However, they also suggest that there is still more work ahead for many plan sponsors and advisors in the Automatic Age.

Retirement Partners Can Help

Get a plan to help improve your 401k results.

Disclosures, Sources, and Footnotes

1 Employees may opt out; in addition, there is an exception for small businesses with 10 or fewer employees, new businesses that have been operating for less than three years and church plans.

2 The Executive Summary of the Society of Human Resource Management’s “2022 Employee Benefits Survey” can be viewed at: https://tinyurl.com/3xpr3sd3.

3 Vanguard’s “How America Saves 2022” can be viewed at: https://tinyurl.com/5c29waxw.

4 Senate Finance Committee, SECURE 2.0 Act of 2022 ; Ariel/Aon-Hewitt study referenced in Section 101.

5 John Hancock’s “State of the participant 2022” can be viewed at: https://tinyurl.com/4ftvxe48.

For plan sponsor use only, not for use with participants or the general public. This information is not intended as authoritative guidance or tax or legal advice. You should consult with your attorney or tax advisor for guidance on your specific situation.

Kmotion, Inc., 412 Beavercreek Road, Suite 611, Oregon City, OR 97045; www.kmotion.com

©2023 Kmotion, Inc. This newsletter is a publication of Kmotion, Inc., whose role is solely that of publisher. The articles and opinions in this publication are for general information only and are not intended to provide tax or legal advice or recommendations for any particular situation or type of retirement plan. Nothing in this publication should be construed as legal or tax guidance; nor as the sole authority on any regulation, law or ruling as it applies to a specific plan or situation. Plan sponsors should consult the plan’s legal counsel or tax advisor for advice regarding plan-specific issues.

Approval Tracking #RP-825-0223 Tracking #1-05362213